The deadlock in between Agile and Waterfall procedures has actually continued job management discourse for years. Software application advancement groups grow in Agile environments, however an absence of management assistance is among the significant challenges to Agile improvement A task supervisor operating in the software application market for any length of time has actually most likely experienced a C-suite that desires them to “do Waterfall.” However exactly what does that mean in practice?

For several years, research studies have actually revealed a favorable relationship in between making use of Nimble structures and job success, and it might be appealing for a task supervisor to think they simply require to offer their business officers on Agile’s outcomes. However it’s similarly essential to comprehend what upper management likes about the Waterfall method If you comprehend the monetary safeguards that Waterfall manages the C-suite, you can craft a hybrid structure that will bridge the space in between Nimble practices and business Waterfall at last. The start of that understanding depends on Waterfall’s primarily unknown origin story.

The Dirty Origins of Waterfall Approach

The majority of people in organizational management associate the term “Waterfall” with the chart below, which originates from “ Handling the Advancement of Big Software Application Systems,” a prominent scholastic paper composed by Winston W. Royce, PhD, in 1970. Royce’s illustration is commonly credited as the very first expression of Waterfall advancement.

The crediting of Waterfall advancement to Royce’s research study is among the odd paradoxes of the software application market. In his paper, Royce never ever utilizes the word “waterfall” or promotes it as an efficient system; he in fact provides what would become referred to as Waterfall as a cautionary tale– an example of a procedure that is “dangerous and welcomes failure” due to the fact that it does not represent the required model required amongst software application advancement phases.

Royce was not alone: 18 years later on, Barry W. Boehm, PhD (who would quickly end up being director of DARPA), utilized an extremely comparable illustration, once again as an example of a troublesome software application advancement life process, and proposed iterative advancement as a beneficial option. In 1996, nearly the whole software application market backed an iterative advancement cycle called the Logical Unified Process (RUP), which was itself a synthesis of finest practices widely acknowledged by software application engineers.

This raises a huge concern: Why would anybody in management push back versus making use of Agile over Waterfall, a structure that given that its beginning has been seen by market specialists and specialists to be at chances with effective advancement practices?

OpEx vs. CapEx: The Financial Case for Waterfall

The factor Waterfall stays in favor needs a little understanding about a company function that advancement groups rarely think of: accounting.

In double-entry accounting, there are 2 sort of costs: functional costs and capital spending (likewise frequently described as OpEx and CapEx). Any expenditure decreases the net earnings of a business, however a functional expenditure– such as lease, payroll, or insurance coverage– decreases it more The cash is invested, and is for that reason no longer on the books. A capital expenditure– such as realty, factory devices, or workplace furnishings– decreases earnings less due to the fact that of an accounting strategy called devaluation, which disperses the expenditure over numerous years. Likewise, as soon as a possession has actually been acquired, it is thought about part of the business’s net worth.

In Between 2000 and 2002– even as the Agile Manifesto was being established– the business world was rocked by a set of significant accounting scandals, beginning with the United States energy business Enron Simply put, Enron (with the supposed complicity of accounting company Arthur Andersen) hid significant losses from financiers by purposefully mishandling functional costs and capital spending. This became part of a bigger plan to fraudulently inflate its earnings, and for that reason increase its stock exchange worth, by billions of dollars.

Soon afterwards, a comparable scandal took place at United States telecoms business WorldCom. WorldCom likewise concealed losses by actively miscategorizing functional costs as capital spending, and the 2002 session of Congress responded by passing the Sarbanes-Oxley Act Consisted of in this costs’s arrangements were brand-new guidelines that made business officers, such as the CEO and CFO, personally responsible for investor losses that took place due to the fact that of an absence of due diligence.

When it pertains to software application advancement, CapEx versus OpEx is a specifically complicated concern: CapEx looks excellent on a balance sheet, permitting business to report a much better operating earnings and obtain bigger amounts.The drawback, nevertheless, is that capitalization requirements have actually developed and need documents, evaluations, and approvals– all of which can considerably prevent the software application advancement procedure.

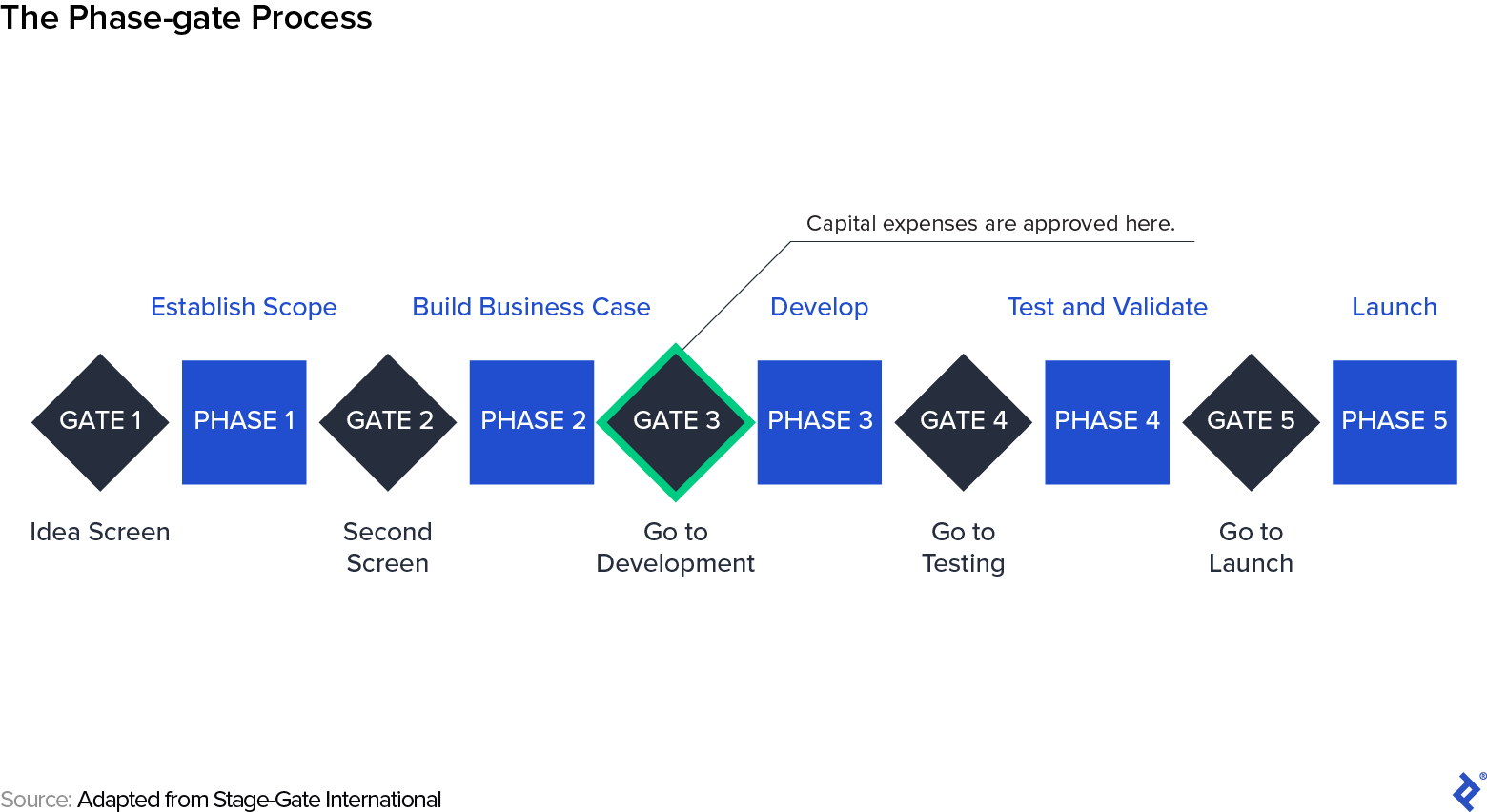

This is where job management plays a main function. In the wake of this legislation, CFOs required a security system that they might indicate: a management design that might show they had actually satisfied the requirements of the Sarbanes-Oxley Act. The Task Management Institute had an option: the phase-gate procedure (likewise referred to as stage-gate). This Waterfall strategy utilizes a series of “gates”– stops briefly where executive approval would be required for advancement to advance. By specifying a phase which contained just CapEx-eligible activity, and separating it from all other phases, CFOs might show that they had actually worked out due diligence when noting an expense as a capital expenditure.

Fast-forward to today day, and phase-gate management has actually been the de facto requirement for advancement tasks at public business for twenty years– Stage-Gate International approximates that 80% of the Fortune 1000 utilizes some variation of this structure. For a Nimble designer or job supervisor, this might appear confusing. Does not your CFO understand the advantages of Agile? They might or might not, however in either case, the most essential thing for a task supervisor to keep in mind is: They do not care.

When the CFO desires you to “do Waterfall,” it’s not based upon a belief that Waterfall is the most reliable method to provide software application. It seldom matters to them if developers utilize RUP, Scrum, XP, Crystal, FDD, DSDM, Kanban boards, or any other advancement strategy or management structure; what they appreciate is capitalizing the job without breaching the regards to the Sarbanes-Oxley Act.

The bright side is that whatever you require to do to guarantee the CFO that the job will pass an audit happens beyond the real advancement procedure. If you can guarantee the C-suite that their requirements will be satisfied, they need to be open to a hybrid method in which monetary issues are dealt with by means of Waterfall in the preparation phase and advancement is performed in a Nimble structure:

Browsing the Falls

If a task supervisor comprehends what their CFO desires and can guarantee them of the functional oversight supplied by a phase-gate structure, there’s no factor to utilize Waterfall over Agile in advancement. Simply approach the requirements of phase-gate management with the understanding that its function is monetary and legal and does not need to affect your group’s advancement work. Here’s how to begin:

Deal With Budgeting as Iterative … Up Until It Isn’t

Every year, the business spending plan assigns a set total up to capital investment. One little piece of that is designated to software application advancement tasks, and magnate work out for the most significant piece possible for their tasks. This settlement procedure normally goes on for the very first 2 or 3 months of the .

Settlement is incredibly iterative, so job spending plans change continuously throughout this procedure. Empower your company sponsor by supplying them with adjustable quotes. The objective here is to develop a budget plan envelope, so broad choices for several contingencies will be incredibly useful. For instance, together with a standard quote, you may supply a less expensive alternative that would be practical if cost-saving conditions are satisfied, like doing information migration by means of manual entry, or a more costly alternative if additional functions are consisted of, like a mobile app. This will assist your company sponsor change their spending plan demand as treasury committee settlements get underway.

These quotes require to be supplied ahead of spending plan settlements, due to the fact that as soon as the treasury committee authorizes the tasks for the year, there is no going back. In the phase-gate system, gate 3 is where the job is provided treasury approval. Versatility in budgeting exists, however just on the front end of the procedure, prior to this gate takes place.

Understand Materiality

Your job control workplace (or, if you do not have one, your monetary controller) can assist you comprehend business limits for materiality— the point at which monetary variation is necessary enough to be tape-recorded: The purchase of a box of pens might be thought about immaterial, however purchasing brand-new computer systems for the group isn’t. The line where immaterial ends up being product differs by business. Comprehending your business’s limit, and recording appropriately, will endear you to anybody making accounting choices.

Share your domain understanding with your equivalent in financing; for instance, comprehending the principle of switching user stories and reaching agreement on how to deal with the practice will prevent the look of impropriety. Guarantee them that if any extra expenditure from a swap threatens to go beyond the materiality limit, you will intensify it so it can be correctly recorded.

Speak the Language of Financing

If you are not currently knowledgeable about weekly status reports and threat logs, get familiar. Read them. Love them. Fill them out frequently and precisely. Provide to your job management workplace and they will like you in turn.

Most notably, if you supply job spending plan reports or updates, ensure your line product titles and descriptions precisely match the ones you utilized when the spending plan was very first authorized. If the authorized spending plan describes “Legendary: Authentication UI,” then that’s what you need to place on your report– not “Legendary Login Screen” or any other variation. Disregard this suggestions and you are ensured to produce friction and aggravation throughout the whole monetary arm of the company.

Worth Delivered

If you satisfy the monetary requirements above, congratulations! You’re satisfying the C-suite’s requirement to “do Waterfall.” The capital spending are correctly tape-recorded, and no part of the procedure has actually needed any modification in how code is in fact composed or how updates are provided. Any compromises you have actually needed to make in preparation have actually acquired you allies in other departments and the C-suite. The procedure has actually likewise provided you a much better understanding of how your group can deal with other parts of the company, instead of toiling in seclusion– or even worse, operating in opposition to those who are expected to be in your corner.

An Nimble perfectionist may think about these monetary issues to be “agreement settlements.” Nevertheless, it’s simply as legitimate to consider your monetary coworkers as internal company consumers. Fulfilling their requirements on matters of financing is simply another type of consumer cooperation. And in Agile, the consumer’s understanding of worth provided constantly wins.