Pleasureofart

Intro

I’m not the greatest fan of development stocks. The stakes are generally extremely high, and prospective earnings depend upon the instructions of rates of interest and inflation expectations. After all, the lower future inflation is anticipated to be, the more appealing it ends up being to mark down future capital.

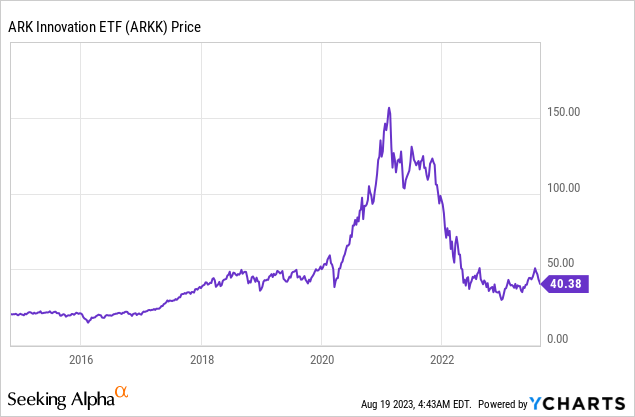

Utilizing Cathy Woods’ ARK Development ETF ( ARKK) as a criteria, we see a huge rise in 2020 and 2021 triggered by (worldwide) absolutely no rate of interest policies, extremely low inflation, and QE to additional assistance liquidity.

In the 2nd half of 2021, inflation began to speed up, triggering a shift in rate of interest expectations. It ended up being more appealing to purchase business with greater earnings (worth stocks), which activated a huge rotation.

This year, ARKK is up 30%, thanks to slowing inflation and expectations that the Fed may be near to its terminal rate.

Nevertheless, it goes to demonstrate how vulnerable pure-play development stocks are, which is why I generally choose a mix of development and worth. Or, as some refer to it as: development at an affordable rate.

User-friendly Surgical ( NASDAQ: ISRG) is among these stocks. The business is among the fastest-growing business on my list. In early July, I started protection of this business due to my increasing concentrate on the health care sector.

Ever Since, we have actually seen an intriguing advancement.

- The business has beaten revenues quotes, treked its assistance, and revealed excellent advancements in the application of its surgical treatment robotics and associated services.

- Wall Street has actually treked its rate projections.

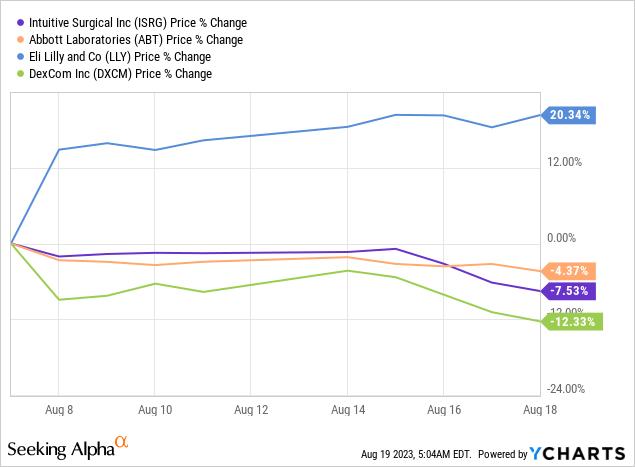

- ISRG’s stock rate is down 18% over the previous 4 weeks.

This stock rate decrease is fascinating, as it offers ISRG a more appealing appraisal and due to the fact that it appears that due to the fact that of the success of weight reduction tablets, the marketplace is anticipating business that (indirectly) gain from the adverse effects of weight problems to lose long-lasting development chances.

Wall Street Journal

In this short article, we’ll concentrate on the brand-new risk/reward for ISRG and what to make from what I think is among the very best development stocks on the marketplace – with an affordable appraisal.

So, let’s get to it!

The Threat Of Weight-loss Drugs

ISRG is among the most remarkable business in health care, as it has actually refined the art of performance in surgical treatments. In this case, the business is riding 2 enormous tailwinds:

- It is at the core of health care development.

- It enhances performances, which lowers long-lasting expenses for doctor. Particularly because of the increasing labor scarcities and increasing expenses, this is essential.

User-friendly Surgical

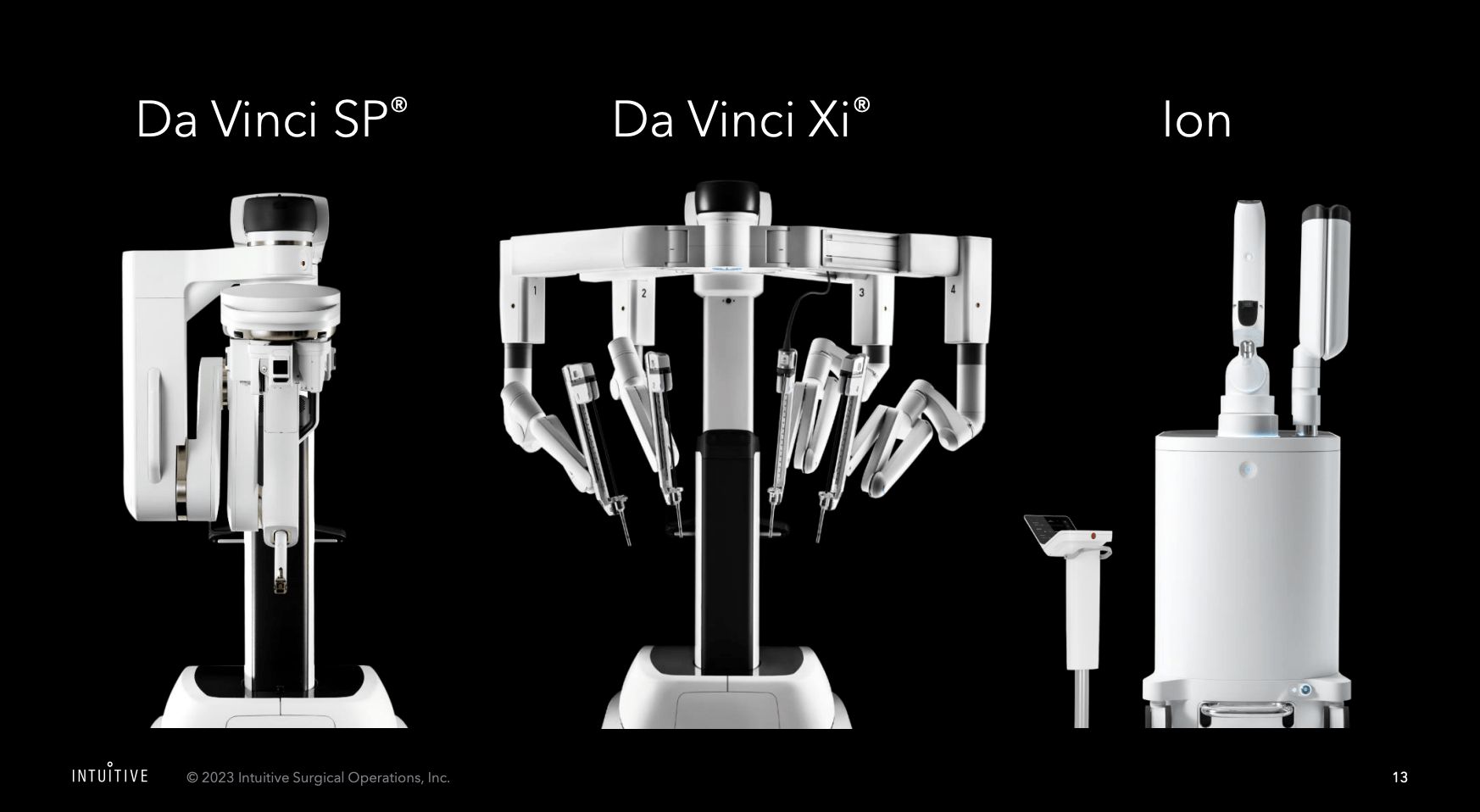

The business produces and offers 3 essential robotic systems, Da Vinci SP, Da Vinci Xi, and Ion, which have actually a set up base of more than 8,000 systems in the United States and abroad.

User-friendly Surgical

According to the business (focus included):

The da Vinci surgical systems are created to allow cosmetic surgeons to carry out a large range of surgeries within our targeted basic surgical treatment, urologic, gynecologic, cardiothoracic, and head and neck specializeds. To date, cosmetic surgeons have actually utilized the da Vinci Surgical System to carry out lots of various kinds of surgeries Da Vinci systems use cosmetic surgeons three-dimensional, hd (” 3DHD”) vision, an amplified view, and robotic and computer system help. They utilize specialized instrumentation, consisting of a miniaturized surgical cam (endoscope) and wristed instruments (e.g., scissors, scalpels, and forceps) that are created to aid with accurate dissection and restoration deep inside the body

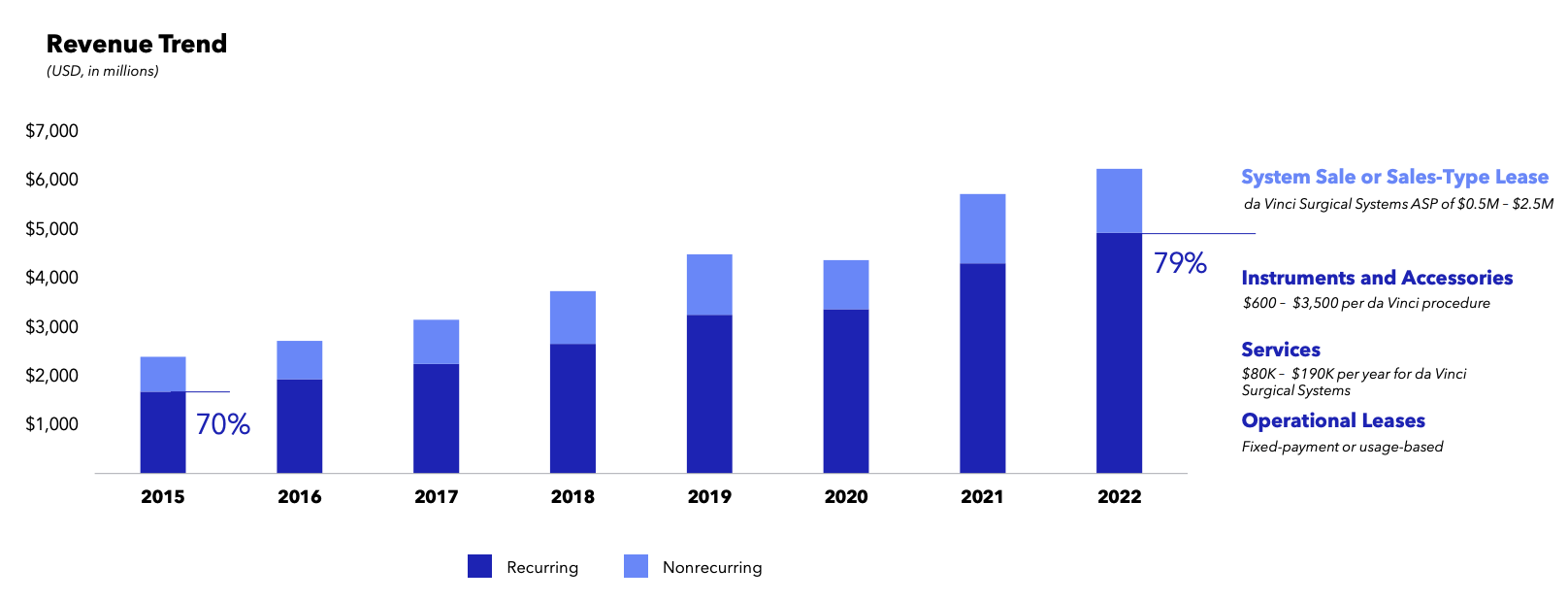

It likewise requires to be stated that an increasing share of its earnings is now repeating, which is an indication that the business generates income for several years after it has actually set up a brand-new system. It’s likewise a quality of a wealth compounder.

User-friendly Surgical

To put it simply, as long as ISRG is the leader in its field, it gains from nonreligious development like an increasing worldwide population, increasing health care requirements, and (this is a lot more crucial, the big requirement for more performance in health care.

Having stated that, weight problems is among the greatest motorists of health care need.

I believe all of us understand that weight problems has actually ended up being a pandemic in the West, resulting in a large range of health concerns (according to the CDC):

- Hypertension (high blood pressure)

- High LDL cholesterol, low HDL cholesterol, or high levels of triglycerides (dyslipidemia)

- Type 2 diabetes

- Coronary heart problem

- Stroke

- Others

As one can think of, the expectation that a marvel tablet can treat weight problems is harming the stock costs of a great deal of business.

Because August 7, ISRG shares have actually lost 8%. Ely Lilly ( LLY), among the business behind the tablet, is up 20%. Other business associated with cardiovascular disease and diabetes are likewise down.

On a side note, revenues calls are significantly pointing out GLP-1 (the name of these drugs):

Bloomberg

Nevertheless, as much as I would like for a tablet to be reliable (I’m not rooting versus the health of individuals to make a dollar on health care stocks), the proof isn’t there yet.

For instance, these drugs are costly, and health companies are cutting gain access to

On top of the high expenses, it is not yet clear what the adverse effects are and what occurs the minute individuals stop taking these drugs. After all, I believe the objective needs to be to fix weight problems without getting individuals hooked on tablets for the rest of their lives.

Dr. Susan Yanovski, a co-director of the workplace of weight problems research study at the National Institute of Diabetes and Gastrointestinal and Kidney Illness, alerted that clients would need to be kept track of for uncommon however major adverse effects, specifically as researchers still do not understand why the drugs work. – NY Times

While the unpredictability surrounding these tablets is clearly putting some pressure on ISRG and its peers, the business is not extremely satisfied by these drugs. Likewise, it’s prematurely to make the case that these tablets can have a significant impact.

This is what the business stated throughout its 2Q23 revenues call:

Some clients have actually shown that they are seeing increased client interest in weight reduction drugs It is prematurely to conclude if the slowing development is a momentary time out as clients assess these brand-new drug treatments or if it is a pattern that continues. Our company believe that throughout the quarter, da Vinci continued to acquire market share in the bariatric surgical market

To put it simply, in spite of the danger of competitors, da Vinci got market share in weight-focused surgical treatments.

Moreover:

What we saw in Q2 was that development rate slowed. We have some input from clients that the level of client interest is such that clients are now thinking about drugs versus surgical treatment It’s uncertain yet based upon that set of inputs from clients, the period of that assessment by moms and dads– clients and clearly it’s layered. So what we provided for our assistance was we simply stated at the luxury, for the rest of the year, the bariatric development rate in the United States follows what we saw in Q2 And at the low end, we stated the development rate continues to slow a bit throughout the year as clients ended up being significantly informed about the weight reduction drugs And clearly, there’s a variety of elements that clients need to think about with regard to those drugs, expense, adverse effects, what occurs if they come off the drugs and gain back weight, et cetera However I believe from our point of view, we’re early in comprehending what the longer-term effect will be. Consumers have actually stated that they have self-confidence that there is a function for surgical treatment in weight reduction which that will withstand over type of the longer term What occurs in for the remainder of the year, I believe we’ll see.

Even if these drugs end up being a video game changer (and I hope they do), I do not believe that the bull case for ISRG is going to be thwarted.

ISRG Continues To Fire On All Cylinders

Given that my last short article, the business has actually reported its second-quarter revenues. The 2nd quarter saw 22% development in treatments, with significant strength in basic surgical treatment and gynecology for benign conditions, especially in the United States.

General surgical treatment treatments like cholecystectomy and hernia repair work were surpassing, and there was healthy development in colon and rectal treatments also.

Worldwide treatment development stayed strong due to healing in China and constant strength in Japan, Germany, and the UK. Ion treatments likewise revealed strength, with a 145% boost.

The increase in treatments can be credited to a stockpile of clients whose treatments were postponed throughout the pandemic.

Moreover, the business kept in mind that brand-new cosmetic surgeons signing up with the da Vinci platform contributed favorably to treatment development, showing the efficiency of training programs and the increasing variety of graduates from residency and fellowship programs trained on da Vinci.

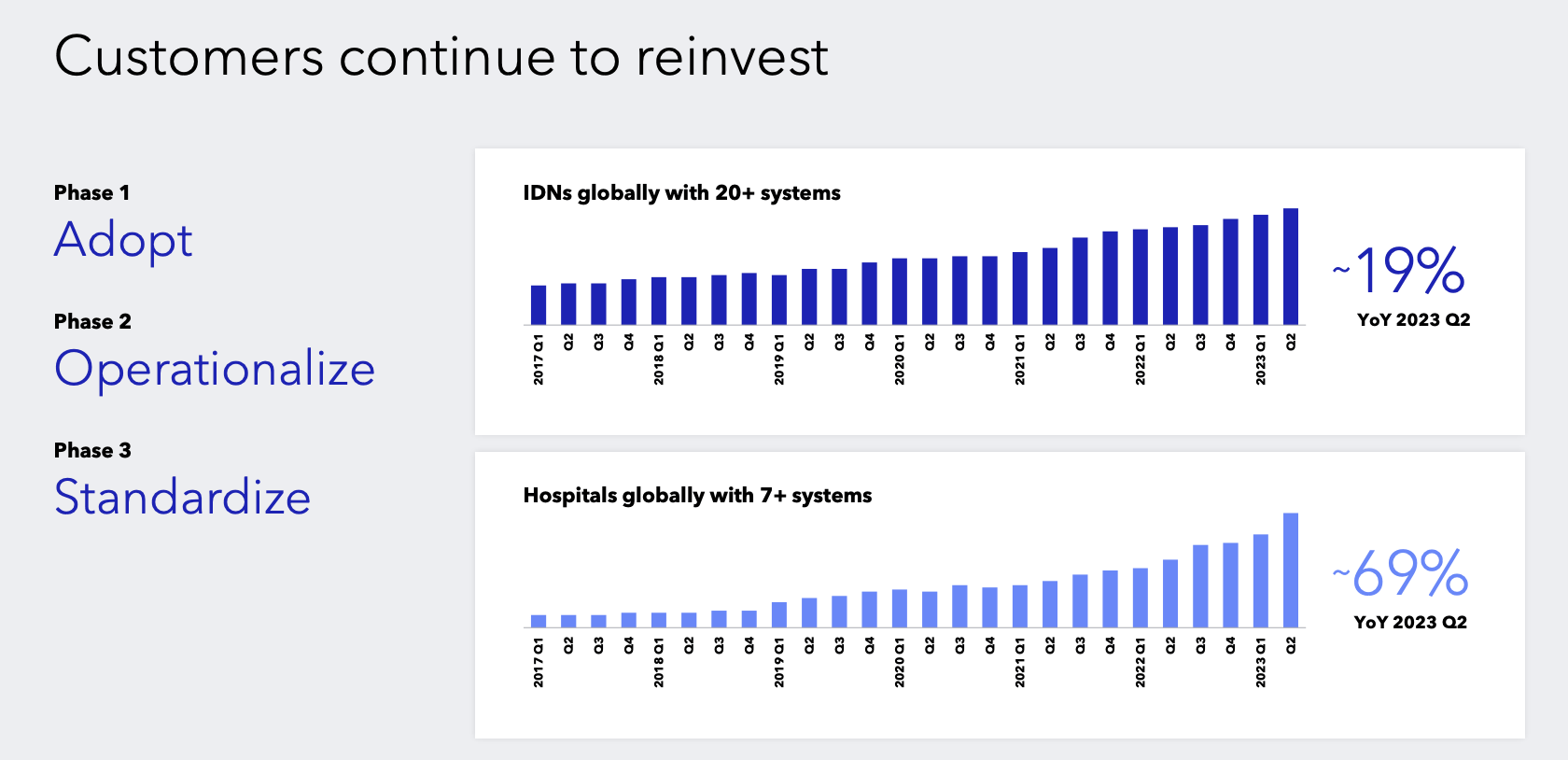

On top of that, the business’s positionings revealed more powerful momentum, with 331 systems positioned in 2Q, compared to 279 systems in the prior-year quarter.

The medical set up base now covers 7,900 multi-port da Vinci systems, 435 Ion systems, and 142 single-port da Vinci systems.

User-friendly Surgical

Nevertheless, it requires to be stated that the business is seeing some headwinds in China.

Throughout its 2Q23 revenues call, ISRG kept in mind that regional rivals’ increasing involvement in tender procedures under the nationwide quota and prices pressure arising from federal government policy modifications and competitors have actually increased unpredictability in the outlook for China’s treatment, system positioning, and earnings efficiency.

Mentioning China, throughout its call, ISRG highlighted current medical research studies.

- A performed in China compared results of robotic best colectomy and laparoscopic best colectomy. The research study covered over 15,000 clients from 42 research studies. The robotic technique showed benefits such as much shorter healthcare facility stays, substantially lower danger of conversion to laparotomy, and decreased problem rates, specifically when thinking about intra-corporeal anastomosis treatments.

- Another research study from Connecticut evaluated the results of robotic-assisted and video-assisted thoracoscopic surgical treatment. The robotic arm displayed lower rates of conversion to open treatments compared to the VATS arm, recommending equivalent perioperative results with decreased conversion danger.

Evaluation

In spite of the danger of weight reduction tablets and increased competitors in China, the business modified its full-year treatment development projection to a variety of 20% to 22%, up from the previous series of 18% to 21%.

This upward change is based upon expectations of continual raised treatment volumes, disallowing considerable macroeconomic obstacles.

The projection likewise acknowledges prospective unpredictabilities connected to bariatric development in the United States, client health care usage, and financial conditions.

- The gross revenue margin for 2023 is forecasted to fall in between 68% and 69%, based on variations driven by item, local, and trading characteristics, along with brand-new item intros.

- Pro forma running expenditure development for the year is anticipated to be in between 12% and 15%, with non-cash stock payment expenditure anticipated to variety in between $600 to $620 million.

- Other earnings, mostly interest earnings, is expected to amount to in between $160 and $180 million, showing the effect of increasing rates of interest.

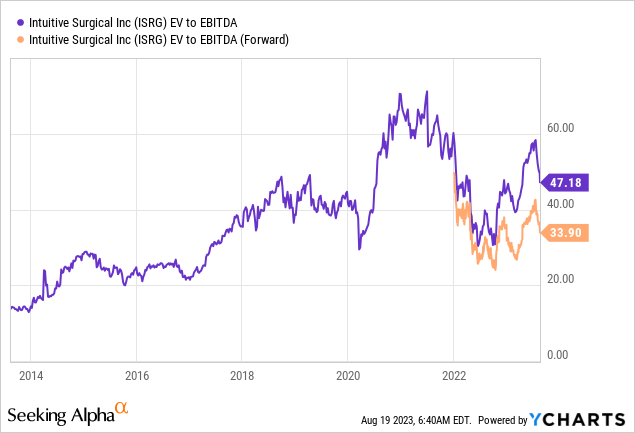

Having stated that, the business is now trading at approximately 34x NTM EBITDA.

While it might look like a raised appraisal, I think the business’s appraisal is appealing. For instance, long-lasting EBITDA development is anticipated to stay near to 14%. There are just a handful of multi-billion market cap business that can take on that.

If we use a 38x EV/EBITDA numerous, I get in between 48% and 60% advantage.

This is based upon a $100 billion market cap and $5 billion in anticipated net money next year. The business has more money than gross financial obligation.

Leo Nelissen (Based upon expert quotes)

This would put the longer-term rate target at $440.

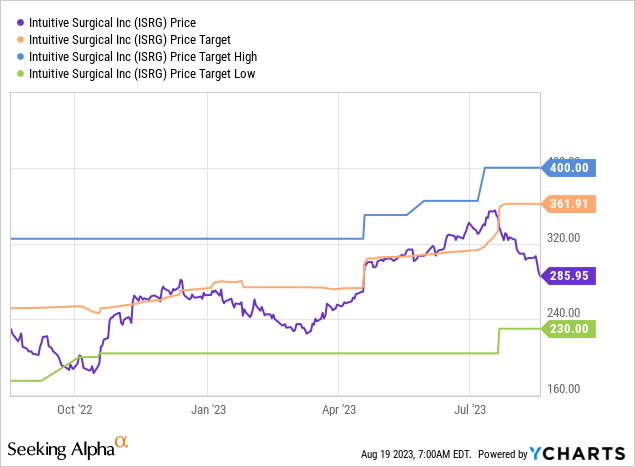

Taking a look at shorter-term targets, we see that the business has actually been updated in current weeks, in spite of seeing a stock rate decrease.

The existing agreement rate target is $362, which is 26% above the existing rate. I concur with that target.

To put it simply, while short-term market unpredictabilities will likely keep a cover on development stocks, I think that ISRG is among the very best development plays in health care, and if this sell-off continues, I might purchase it – in spite of my concentrate on dividend (development) stocks.

Takeaway

Operating in the ever-evolving health care sector, ISRG flourishes on 2 critical motorists – pioneering health care development and boosting performance to minimize long-lasting expenses for companies. Its 3 robotic systems, consisting of Da Vinci Xi and Ion, have actually currently added to more than 1.8 million treatments.

While weight reduction tablets produce ripples in the market, ISRG stays durable.

As clients check out these drugs, the business’s fortress in the bariatric market continues.

In the middle of worldwide unpredictabilities, ISRG stays strong as it publishes strong development in treatments, worldwide positionings, and development. The numbers inform an engaging story, and the stock’s current dip uses an appealing entry point.

If the existing sag continues, I’m keeping a close eye on ISRG for prospective addition in my portfolio.