mphillips007

The Hershey Business ( NYSE: HSY) showcased a robust enhancement in Q3 2023 monetary outcomes, highlighted by a considerable uptick in net sales. This excellent development was mostly credited to an increase in natural sales, which originated from tactical rate modifications targeted at countering inflationary pressures. Hershey’s skilled handling of rates and expense control techniques appeared. Additionally, the business saw a notable increase in its gross margin, suggesting its effective steering through the increased costs connected to production and basic materials. This piece supplies an extensive monetary and technical evaluation of the stock rate to determine its upcoming trajectory and determine prospective financial investment chances. It has actually been kept in mind that the stock is presently going through a correction stage, which financiers need to consider as a prime financial investment chance.

Monetary Rise with Strong Sales and Revenue Development

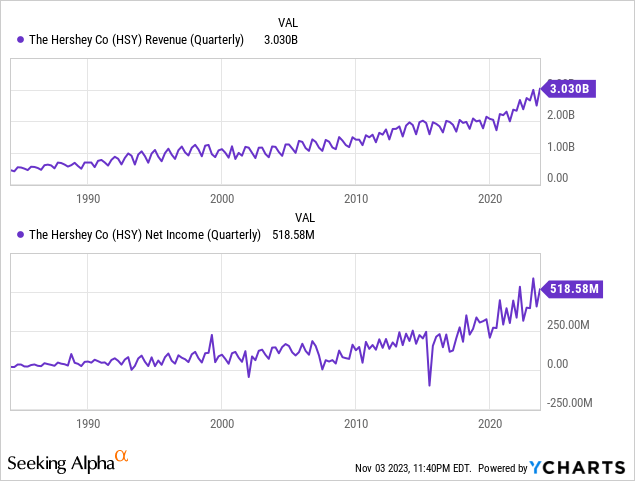

The Hershey Business showcased a strong monetary standing in Q3 2023, with overall net sales intensifying by 11.1% to $3.03 billion. The uptick was mainly driven by a 10.7% boost in natural net sales on a continuous currency basis. Volume increments were minor however deliberate, underpinned by prepared stock boosts within the North American Salty Snacks department in anticipation of the brand-new ERP system launching in early October. Hershey’s tactical rates procedures resulted in a noteworthy gross margin elevation, skyrocketing from 40.6% in Q3 2022 to 44.9% in Q3 2023, marking a 430-basis-point rise. This highlights Hershey’s skilled management in rates and effectiveness improvements that expertly reversed increasing expenses in production, basic materials, and basic overhead.

The business’s increased earnings was consulted with disciplined cost management, although it came to grips with raised selling, marketing, and administrative expenses, which saw a 13.1% year-over-year climb. This was generally due to a 20% boost in investments for marketing and customer marketing, showing Hershey’s magnified financial investment in its brand name portfolio. Nevertheless, Hershey was successful in keeping a tight rein on general costs, which saw a moderate increase of 9.9% when leaving out marketing and advertising expenses, matching the results of wage and advantages inflation, along with ability and innovation financial investments. The chart listed below screens Hershey’s quarterly earnings and earnings, showing a noticable upward pattern in success.

Hershey’s operating revenue for Q3 2023 stood apart incredibly, with a dive of 32.2% to $735.9 million and running revenue margin development of 390 basis indicate 24.3%. The adjusted operating revenue likewise illustrated a resilient situation, climbing up by 22.4% to $753.4 million, with the margin widening by 230 basis indicate 24.9%. These revenue escalations were backed by the business’s skilled rate awareness and effectiveness gains, which more than made up for the intensifying expenses associated with brand name promo, acquisition-related expenses, and the wider inflationary scene.

For 2023, Hershey prepares for a net sales development of roughly 8%. The business anticipated a reported EPS development of 13% to 15% and an adjusted EPS development of 11% to 12%. The business has actually changed its general tax outlook, anticipating a somewhat greater financial investment in tax credits, leading to a reduced tax rate compared to previous forecasts and an efficient tax rate of around 15%. Furthermore, Hershey is set to sustain an “other cost” of about $225 million to $230 million, generally due to the write-down of equity financial investments qualified for a tax credit. Interest costs are forecasted to be around $155 million. The company likewise prepares to invest in between $800 million and $850 million in capital investment, mostly concentrating on increasing its core confection capability and advancing its digital facilities, that includes presenting and improving a brand-new ERP system throughout the business.

Conclusively, Hershey’s robust monetary efficiency in Q3 2023, identified by substantial sales development and margin growth, shows the business’s tactical acumen in browsing market obstacles and purchasing development. With disciplined financial management, financial investment in brand name and facilities, and proactive adjustment to vibrant market conditions, Hershey is well-positioned to sustain its upward trajectory in success and investor worth.

Checking Out Technical Cost Structures

The technical potential customers for Hershey appear extremely positive, as evidenced by the regular monthly chart listed below. Following a robust healing from the Great Economic crisis, the rate has actually skyrocketed, climbing up 1169.37% from its 2009 low of $21.61 to an unmatched peak of $274.31.

This strong rally was because of tactical service choices and wider market patterns. Post the monetary crisis of 2008, Hershey invested greatly in marketing and broadening its item lineup, which assisted the business catch a bigger market share. Their concentrate on brand name strength and customer commitment settled, as the business had the ability to take advantage of its renowned brand names to drive sales. Additionally, emerging markets supplied brand-new development opportunities as Hershey profited from increasing non reusable earnings and a growing cravings for confectionery items. Hershey’s strong supply chain management and rates techniques likewise played a substantial function in improving success, which, in turn, boosted financier self-confidence and increased the stock rate.

Hershey Month-to-month Chart (stockcharts.com)

Furthermore, Hershey’s stock rate experienced a substantial increase from customer buying patterns driven by the pandemic and the business’s creative modifications to the brand-new market conditions after 2020. As customers stockpiled on home cooking and treats throughout lockdowns, Hershey’s items saw an uptick in need. The business’s swift pivot to e-commerce and digital marketing enabled it to reach customers even as conventional retail channels were interrupted. Furthermore, Hershey’s continuous dedication to sustainability and social obligation efforts started to bring in a growing section of socially mindful financiers. The low-interest-rate environment post-2020 likewise contributed, as financiers looked for haven in stocks with steady dividends and resistant service designs, even more pumping up the stock rate in the middle of an unstable market.

After Might 2023, Hershey’s stock rate dipped as customer costs moved far from confectioneries to important items in the middle of increasing inflation issues. The business likewise dealt with supply chain disturbances that resulted in greater production expenses and afflicted revenue margins, triggering financiers to reassess the stock’s evaluation. Additionally, a cooling off of the pandemic-era need for home cooking led to minimized sales projections for Hershey, causing a bearish belief amongst financiers and an ensuing drop in the stock rate.

This substantial rate drop has actually been under substantial stress, as evidenced by the regular monthly candle lights for the previous 6 months. This down pattern was started from a peak of $274.31 and has actually been on a consistent slide, approaching crucial assistance limits. The Fibonacci retracement levels from 2009 to 2023 suggest that the 38.2% and 50% retracement levels are placed at roughly $177.78 and $147.96, respectively. These levels are considered to be robust assistance zones. As the rate approaches the 38.2% Fibonacci level, there is capacity for a considerable bounce in the stock’s worth. Furthermore, the ongoing down pattern towards the 50% retracement mark may experience the supreme assistance, setting the phase for a possible upward rise.

Secret Action for Financiers

To acquire a much deeper insight into the robust bullish belief surrounding Hershey, the weekly chart listed below provides the rate under oversold area. It shows rates pressure, yet an inverted head and shoulders pattern in 2020 strengthens the bullish belief. The head of this pattern lies at $102.61, with the shoulders at $128.60 and $126.56. This recommends that any current rate pullback need to be viewed as an engaging purchasing chance for financiers. The levels at $177.78 and $147.96 are recognized as considerable assistance zones, providing beneficial entry points for financial investment. It is recommended for financiers to start positions at $177.78 and to think about increasing financial investment if rates decrease to $147.96. Furthermore, the weekly chart’s RSI signals an oversold condition, which might foreshadow a possible rate healing from today levels.

Hershey Weekly Chart (stockcharts.com)

Market Threat

Hershey’s monetary strength in the face of increasing production and basic material expenses suggests a strong market position, yet the business is not invulnerable to wider financial pressures. The uptick in basic and administrative costs, consisting of a 20% boost in marketing and advertising investments, shows an aggressive financial investment in brand name and market share that might be at threat in a financial decline where customer costs agreements. While the business’s disciplined cost management and tactical rates have so far efficiently countered these increasing expenses, there’s a fundamental threat needs to inflation continue or intensify, possibly squeezing margins if rates can no longer be raised without impacting need.

Worldwide, Hershey deals with currency threat, as variations in currency exchange rate might negatively impact the worth of its abroad sales and earnings. Additionally, the dedication to substantial capital expenditures-between $800 million and $850 million-to boost confection capability and digital facilities, while vital for development, provides short-term monetary dangers. Such significant financial investments in the face of unpredictable financial conditions might strain capital. Technical analysis recommends a possible bearish pattern for Hershey’s stock, with vital assistance levels recognized by Fibonacci retracements being checked. Yet, if the rate falls listed below $147.96, it will weaken the favorable pattern and signal extra down motions in rate.

Bottom Line

Hershey’s most current monetary outcomes highlight a business that has actually expertly browsed a complicated financial landscape to provide excellent development. In the face of inflationary pressures and increased expenses, Hershey has actually shown an eager capability to handle costs and carry out tactical rates modifications, leading to a robust improvement of net sales and running earnings. The disciplined method to cost management, combined with tactical financial investments in production capability, digital facilities, and brand name promo, highlights the business’s dedication to continual functional effectiveness and market growth. Regardless of the substantial rate drop in 2023, the long-lasting projection is positive, reinforced by strong assistance levels at $177.78 and $147.96. Financiers might think about purchasing $177.78 and increase positions if the rate dips to $147.96, anticipating a future uptrend in worth.