Black_Kira

When I started to have a look into Ecopetrol S.A. ( NYSE: EC), I was most amazed by the expert agreement. Out of the twelve experts I see covering the name, I just saw one expert with a buy ranking on the story. Ecopetrol is the biggest and most dominant oil and gas business in Colombia and remarkably, it’s not a one-trick pony. Today, over 20% of its company is from activities that do not straight consist of hydrocarbons and by 2040, this number is set to function as EC gradually weans itself far from oil and gas. At the time of composing, the stock is trading listed below its historic assessment levels in spite of EC continuing to publish strong operating and monetary outcomes.

Business Introduction

In 2003, Colombia reorganized its main petroleum business, Empresa Colombiana de Petróleos, changing it into Ecopetrol S.A. The federal government intended to globalize and improve its competitiveness in the oil market. With Decree 1760, dated June 26, 2003, Ecopetrol ended up being an entirely state-owned public corporation connected to the Ministry of Mines and Energy. This modification released the business from its previous function as the oil source administrator, entrusting those obligations to the freshly formed National Hydrocarbon Firm (ANH).

Ever Since, Ecopetrol has actually run more autonomously, concentrating on speeding up expedition efforts, attaining outcomes with a business-oriented technique, and intending to enhance its position in the international oil market. Its global footprint encompasses the Gulf of Mexico, with workplaces in Houston, Texas, and operations in overseas locations in Mexico (Veracruz, Tabasco, and Campeche) and Brazil (offshore, with workplaces in Rio de Janeiro). The federal government of Colombia still preserves an 88.49% ownership stake in Ecopetrol today.

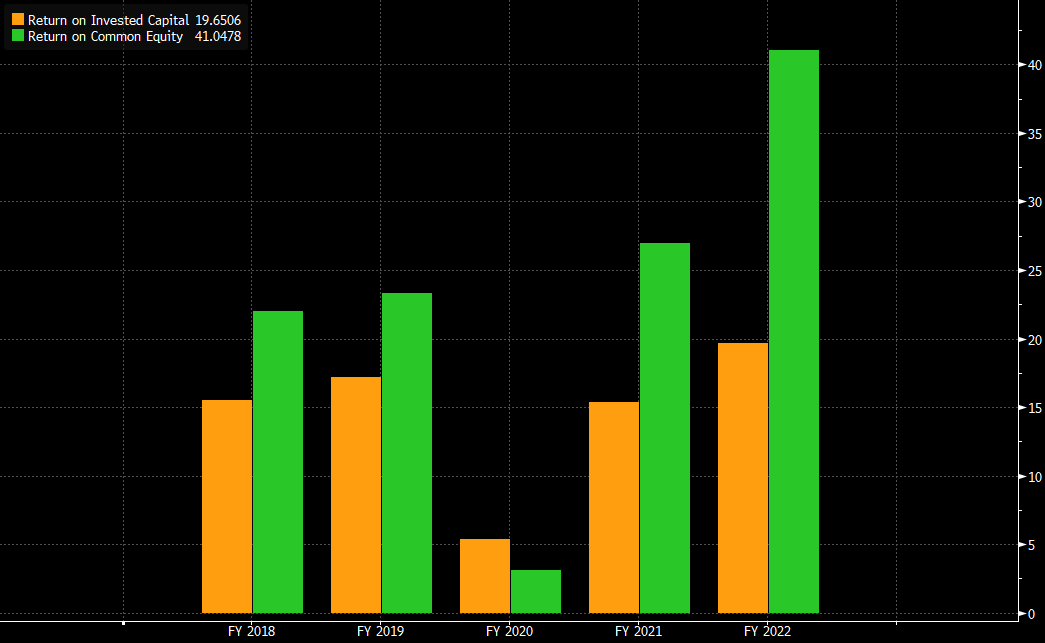

Capital effectiveness has actually been the mantra

Over the previous 5 years, the strength of EC’s concentrate on capital effectiveness has actually produced strong monetary outcomes. These are most apparent when taking a look at EC’s return on equity (ROE) and return on invested capital (ROIC).

Bloomberg

The business has actually been balancing double-digit returns on invested capital and ROE in excess of 20% with the exception of 2020.

Checking Out 2024 and beyond, the expectation needs to be of ongoing capital discipline. Just recently, Ecopetrol exposed its approaching financial investment strategy with a decreased Capex of COP23-27 trillion for 2024, below COP25-30 trillion in 2023. The projections for Upstream (725-730kbpd) and Refining output (420-430kbpd) stay the same. Paired with the business’s Brent quote of $75/bbl, this is anticipated to yield a typical EBITDA margin of 38%. This forecast is a little lower compared to the 40% margin assistance for 2023 with Brent at $80/bbl. The strategy goes for almost the same production figures together with a little minimized CAPEX.

Margins to stay strong in spite of lower oil rates

With a predicted reduction in Brent to about $75/bbl (below around $80/bbl in 2023), Ecopetrol’s 2024 Financial Strategy intends to sustain existing return levels, targeting a somewhat lower ROCE of around 9% compared to in 2015’s 10%. The expected EBITDA margin is around 38%, a decrease from 40% in 2023 however in line with the five-year average. Ecopetrol visualizes transfers to the Country surpassing COP38 trillion (compared to COP40 trillion in 2023) and financial investment levels varying from COP23-27 trillion (compared to COP25.3-29.8 trillion formerly).

Ecopetrol preserves its focus on Expedition and Production (E&P), assigning 62% of its financial investments to this sector. Within Oil and Gas E&P, 50% and 12% of the overall strategy are designated, respectively. The business’s objective is to reach production levels in between 725-730kbpd, a minor boost from 720-725kbpd in 2023. This consists of drilling around 360 advancement wells, with 74% in Colombia and 26% in the Permian Basin, together with an approximated 15 expedition wells, mainly located in Northern Colombia and the Caribbean overseas area.

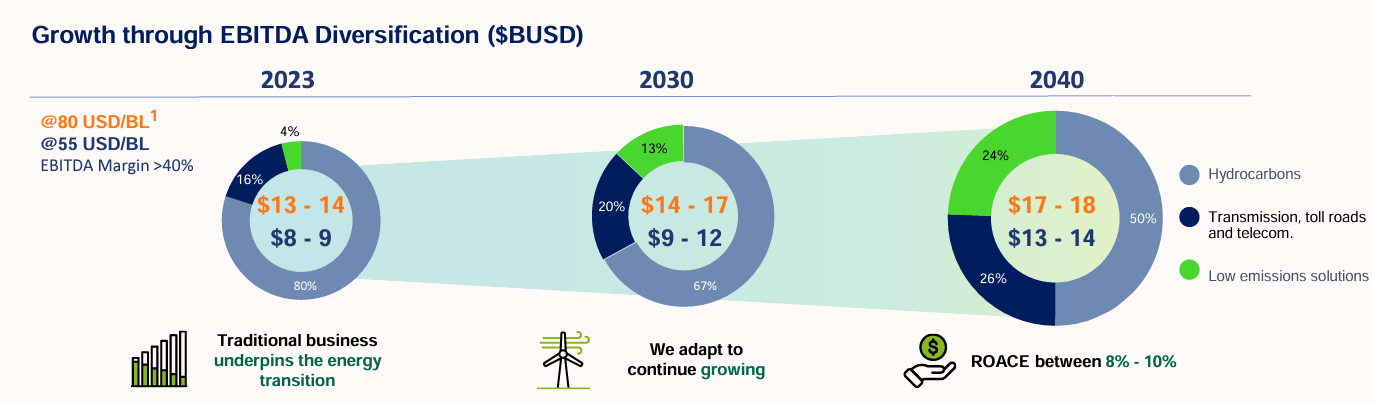

The overarching style of the 2024 strategy is the ongoing concentrate on preserving the success of business in spite of lower Brent rates while likewise concentrating on its support company of hydrocarbons. There are continuing financial investments continuous into its non O&G side of things which must lead to EC doubling its direct exposure to non-extractive organizations by 2040.

Business Filings

The business targets a payment to investors of ~ 75% of its revenues through dividends and to that end, investors have actually gotten $2.81/ share of routine and unique dividends which is not too shoddy thinking about the existing share cost of ~$ 12/share.

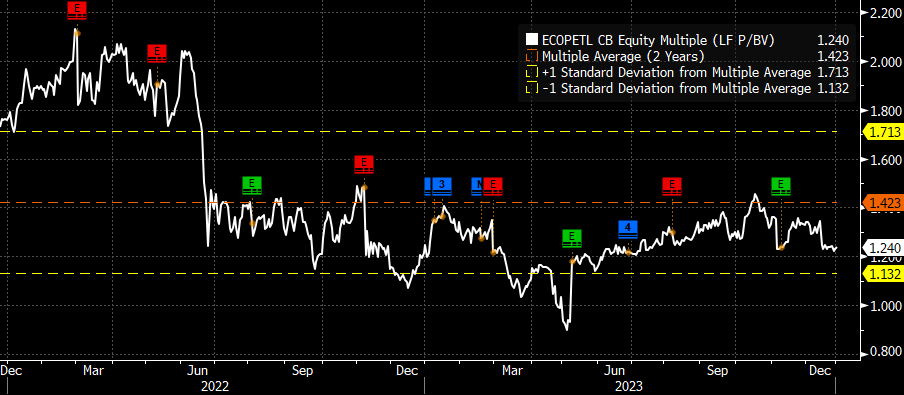

The evaluations make an engaging case for EC

I get back at more bullish on EC when taking a look at it from an assessment lens.

Bloomberg

Regardless of a strong efficiency in 2023, the business trades at a discount rate to its historic Rate to Reserve. EC is presently trading at 1.24 x versus a two-year average of 1.42 x.

Bloomberg

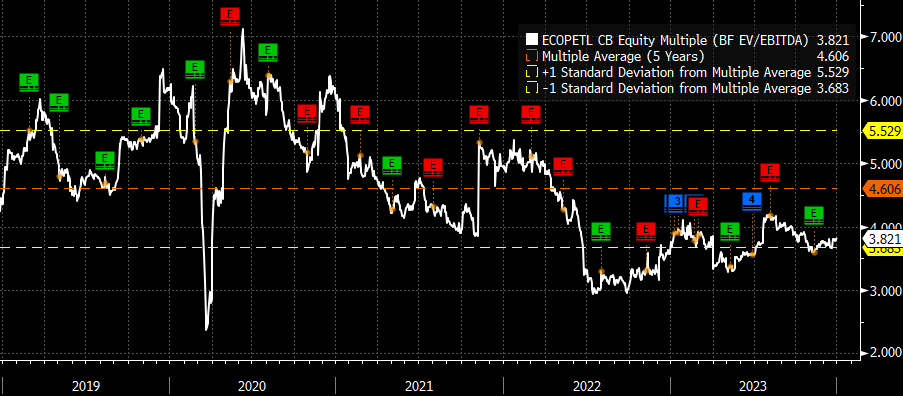

Likewise, EC is presently trading at a lower end of its evaluations on a EV/EBITDA basis. EC presently trades at the lower end of its five-year EV/EBITDA variety.

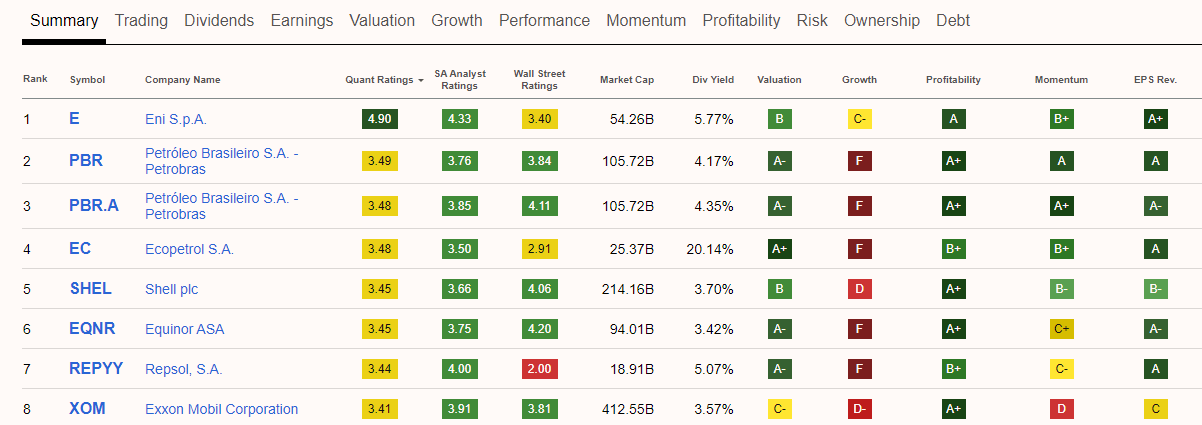

A crucial factor for the unfavorable expert state of mind towards EC is their development profile, or rather the absence thereof. This is currently priced into the stock in my viewpoint. When seeing the name through the Looking for Alpha quant rankings, it evaluates rather well, ranking fourth out of the 16 names in the big cap incorporated oil and gas universe.

Looking For Alpha Quant Rankings

It need to be kept in mind that EC ranks ahead of leviathans like Shell and Exxon, partly due to its assessment and partly due to incomes being modified upwards.This goes to my preliminary point about the expert neighborhood being too sour towards this name. The negativeness towards this name has actually made it simple for the business to shock to the benefit of late.

What can go right?

There is space for this assessment to look a lot more less expensive must we get greater product rates. As specified previously, EC is anticipating a Brent cost of $75/bbl versus $80/bbl in 2023. There is excellent take advantage of to increasing oil rates in EC’s company design.

A positive situation might emerge from:

- Enhanced lifting expenses or lower breakevens, resulting in improved margins.

- Increased volumes or oil rates exceeding expectations.

- A more robust financial rebound in Colombia, leading to greater refinery usage rates.

Any of these circumstances would improve EBITDA upward and make the stock even less expensive versus its existing assessment.

What can fail?

Inversely, nevertheless, we might see EBITDA come under pressure needs to Brent trade lower than presently anticipated. Another element of threat worth pointing out remains in the Permian where EC runs. Needs to production stop working to fulfill expectations, it will adversely affect the business’s success.

The 88.49% stake in EC held by the Federal government of Colombia is a cause for issue for some investors. There is constantly a possibility, that a person day a socialist federal government enters into power and looks for to reassert control over the whole business by leveraging their existing position in the stock.

Often it’s excellent to be a contrarian

I think that the sell-side is too unfavorable on EC. The business’s company design is durable to lower oil and gas rates and its position in the Colombian economy is dominant. With just 1 out of 12 sell-side expert ranking this a buy, I believe the contrarian trade here is for financiers to take a look at more positive circumstances in this name. With evaluations near trough and an investor friendly design, EC might be a lucrative financial investment for financiers particularly if we get greater Brent rates and evaluations reassert themselves to historic levels.